A few of my favorite things... Next week I'll visit the Decorator Showcase house to get new ideas and inspiration for my listings. Get your tickets at decoratorshowcase.org soon! Hope your May is great.

Penthouse Lifestyle, Neighborhood Vibe

Impressive penthouse-living without the dues. This single family home has a marvelous floor plan that is open and generous – entertain on the main floor, retreat to the bedrooms on the second floor. The natural light is abundant and your eyes will dance to the shadows the sun casts throughout. Newer modern west-facing deck with full sun and prized views. The grandiose upstairs has a dreamy master suite with a walk-in closet and a custom window that flaunts the awe-inspiring Bay, San Francisco, Downtown Oakland and Bay Bridge views.

When I took this listing in April of 2017, this well-loved home was in need of updating. The kitchen was worn and all original from 1974, the floors downstairs were original entry tile and old carpet, the master bathroom had seen better days, and the deck was deteriorated and not safe, just to name a few immediate tasks. This home meant the world to the Wang Family so they wanted to present this property in it's best light.

The first task as their Realtor was to determine the property's condition. Before any of my clients invest in cosmetic updates, I always advise them to get current inspections from highly regarded professionals. I would hate for clients to invest money into their homes when there could be significant structural or system repairs needed that could devalue the property.

After inspections are performed, I review the findings with my clients and determine what repairs will yield the best return on their investment. Once my list is prepared, I help my clients obtain bids for said repairs/improvements and work with my clients to create an action plan.

In this case, I envisioned taking this 1970s home and making it sexy, yet comfortable. One of the biggest assets of this home is the panoramic views of Oakland, the Bay, San Francisco and the Golden Gate and Bay Bridges. The deck was in hazardous condition, so engineer Monte Stott was hired by my clients to design the rebuild. After calling six contractors to rebuild the deck, my clients were able to secure a contractor to remove one pier-and-post deck off the living room and remove one cantilevered deck off the master bedroom. The deck off the living room was upgraded with a stainless steel cable with Redwood railing, and the upstairs deck was removed altogether and replaced with a custom 110-inch picture window. The old carpets that had seen decades of life were removed and solid Red Oak floors were installed downstairs. With the exception of the original tile entry and the tile in the powder room, the entire downstairs was transformed to natural finish floors giving the large space a cohesive feeling.

A few likely original 1970s brass track lights remain in the house, but the majority of the interior light fixtures were replaced with groovy West Elm fixtures. Some of the dying juniper shrubs were removed and a few drought-tolerant plants were added to the front yard, such as variegated Phormium. The inside and outside of the property were painted with Benjamin Moore paint, with the exception of Kelly Moore paint on the interior ceilings. 5 1/2-inch solid wood baseboard with no edge detail was added to add a pop to the clean design. The original 1970s geometric railings and the old Harvest Gold double oven give a nod to the decade it was built.

WHEN A GOOD BUY IS NOT A GOOD BUY

Recently I was hired to sell a home. Two years ago it was on the market but it did not sell. At the time the listing agent recommended $45k+ in marketing preparation which the sellers did. From what I understand, an offer came in but it was $200k-$300k less than what the listing agent said the house was worth, so the offer was rejected. The owners decided to rent the property out and, fast forward 2 years, they now want to sell again. As I viewed the lovely home and shared my honest opinion, the owners stated that they got a good deal on the property. I looked up the listing from their purchase and noticed it was on the market for more than two months in a strong seller's market. So my question was, what is a "good deal"?

Is getting a home at listing price when all other homes are selling well over the asking price a good deal? Maybe. You have to compare apples to apples. Perhaps the homes selling for more in the same neighborhood are in better condition, have generous rooms, have great indoor/outdoor space, and the property that is a "good deal" does not.

Let's say a home fits your budget and is cute, however, the surrounding area has challenges. It's important to think about future resale. If you decide to sell in the future and are in an outskirt neighborhood, and perhaps a softer market, your adorable home may get passed over due to someone opting for a better location. Another example is buying on a high-traffic street. It is highly likely that buyers will opt for a side-street or quiet street if given the choice.

Many of my buyer clients say to me "are you trying to talk me out of buying this home". I do not try to talk anyone in or out of buying a home. I want to point out the assets and challenges of any potential property of interest so you can be a savvy buyer. The wrong time to hear about a property's flaws is after you have purchased a property and are later trying to sell it.

Here are a few buyer tips:

- Do not buy with fear as a driver. Meaning, don't be in the mindset of "if I do not get a house now I will never be able to own a home in my lifetime".

- Location. Do not get caught up on staging and the superficial appeal; many items can be fixed, including foundation. However, you cannot move a home's location nor alter flaws you can't change, i.e., no off-street parking, extraordinarily small rooms, an apartment building adjacent to a home or being on an earthquake fault line.

- Are you settling? Ask yourself the tough questions. Really hone in on why you want a particular house.

- Sacrifice. Live with granny's kitchen and awful carpeting if that means you get a home in a desirable area, do not get caught up on the "new updated kitchen".

- If a house has been on the market for a long period of time ask yourself "why?"

What Buyers Need to Know When Viewing Open Houses

If you are shopping for a house you may feel like you are overwhelmed with questions or uncertainty and have anxiety over the unknown. It is helpful to work with an experienced buyer's agent. If you attend open houses without your agent, here are a few tips to keep in mind:

- Any agent hosting an open house, whether they are the listing agent or not, should be helpful and honest with you; however, their fiduciary duty is to get the highest and best for the seller. Don't ask a listing agent what they think the house will sell for. Frankly, they likely do not know and they do not want to scare away any buyer by saying, "I hope we make a record-breaking sale for the neighborhood and it goes hundreds of thousands over the asking price".

- If you do talk with the open house host, other potential buyers are listening and are "sizing up" their competition. It is like poker, do not show your hand. One time I had a buyer tell a listing agent what their budget was and asked the listing agent if they thought they could win the property in competition. Don't do this! You just showed your hand.

- If you ask the hosting agent question after question, you may be conveying the wrong message. Yes, buyers deserve answers to their questions, but let your agent do the research and ask on your behalf. You could be inadvertently sending vibes to the hosting agent that you are uncertain about the house, have grave concerns about the property condition or that you may not be a deal closer. For example, I had a buyer client ask a listing agent about plumbing and water pressure. My client noted that she loved her showers in the morning. My clients called me that night to tell me that they found an old farmhouse that they loved. I immediately called the listing agent to ask for the disclosures/reports on the property. The listing agent immediately remembered my clients and said, "I do not think this is the right house for your clients." I asked, how so? The agent replied that it was a 100-year old home with old pipes and she could not guarantee that the water pressure would be sufficient. Pipes can get replaced and no home is perfect. I was able to discuss at length the property condition with my buyers and inform them about what is typical when reading the disclosures. Buyers may not be aware that certain comments to the listing/hosting agent will convey details that could be possible deal-killers.

- Many Realtors host open houses actively and legitimately to seek out buyers. They may ask guests to "sign in". You don't want to do this if you are already working with an agent. This is a way the host can contact you and solicit your business. Kindly tell them you are working with an agent and give your agent's name. You can always say "I will take your card and ask my Realtor to contact you if we are interested". Some may think there is an advantage to working with the listing agent as their buying agent. But ask yourself, if a conflict arises, would you be comfortable with the same agent representing both sides?

- Don't ask the listing/hosting agent for a showing. Call your agent to set up a private showing. Likewise, when perusing homes online, don't request a showing via online real estate websites. Realtors pay to be sponsor-agents on various websites. If they show you a property that you later purchase with your agent, they can claim they are entitled to the commission; this is called procuring cause.

- While viewing open homes, social courtesies apply. I have seen open house visitors act in way that appears defensive or even hostile. You don't need to engage in long conversations with the host or disclose a lot of information about yourself. Listing agents do remember the visitors and will convey to their seller what their impression is of the buyer.

Bottom line, choose your buyer's agent early in your house hunting process. If you are working with a stellar agent they will do research, talk with you about comparable sold data and pricing, review and discuss property condition, and provide you with answers to your questions. They should be putting your needs above all else and be transparent. Bring all of your questions, concerns and fears to them with full confidence in their advice.

Favorite Things: No. 2

Summertime in the East Bay is unparalleled! Here's a list of my favorite things to savor the season. What are your favorite things for summer?

Words for Buyers

With all of the online tools available today, many new buyers feel that they have a grasp of the market and don’t need the help of an experienced Realtor to assist in navigating the market.

The other night I was talking with a client who was seriously considering submitting an offer on a property in North Oakland. The home checked off nearly all of the boxes on her needs list and we were knee-deep in analyzing the property disclosures. As her advisor, I pointed out the flaws while also sharing with her the reasons I liked the place.

The house had an open floor plan and some thoughtful improvements, while maintaining the essence of its 1908 construction. The downside was that some of the finishes were inexpensive and already showing deterioration; additionally, it could use a bit more storage. We both commented on how we couldn't believe that the sellers didn't deep clean or paint the property in preparation of the sale. (Sellers, yes it is just paint and carpet cleaning but this conveys a lack of care and pride to buyers).

Just three weeks prior, this client wrote an offer on a home that she adored and made her giddy with excitement. She had put in a killer offer on the place but didn't prevail. The heartbreak of not winning was real and the disappointment was tangible.

As we were talking last night, my client spoke about the house she didn’t win in comparison to the house that she was potentially writing on today. I explained that the property that she lost on had sold for more than $100,000 over her budget and was potentially worth $400,000 more than the current house in question. It was indeed a dreamy property that received more than 20 offers. I gently said that although we still covet the house lost (I covet it too) it was not attainable. I suggest that we focus on properties that are attainable.

Think of it like this, there is a handsome man, who is smart and funny. He is flirting with you and gets your heart racing. The only catch is, he is married. He is a big tease and you can't have him. Let's put him back on the shelf and look at real candidates; ones who are genuine, may not be as sexy at first glance, but with a wardrobe makeover could be even better.

Losing out on properties can be an emotional roller coaster. It taps into emotions that often surprise us. It can be a combination of real disappointment coupled with anger. Anger that you work very hard to be able to buy a home and how dare this real estate marketplace be so expensive! Don’t get caught up in the tease. Focus on real candidates that are fulfilling, attainable and will give you true joy. Let the flirts be a fantasy and inspiration on your Pinterest board. Buying a home is a process requiring true focus.

My job and experience is to help you streamline your search. I help organize (and re-organize) your shopping list, explain the nuances of the market and provide inspiration on how you can make your ordinary home magical for you. I know that house hunting requires real support, if you are house hunting right now, hang in there.

Why Timing the Market Rarely Works

I have several clients who are genuinely concerned about over-paying in this market. I completely understand this concern and in no way disregard it. Frankly, the money is not mine, so the purchase needs to make sense for the buyer. The problem is that Oakland and Berkeley have very limited inventory. In Rockridge, only 56 homes sold through the local Multiple Listing Service for the entire year of 2016. If you purchased in this market, you likely paid what you felt was a premium to get into the neighborhood. Maybe you waived your contingencies and paid more than the appraised value. You may be sitting here thinking, "Who does Deidre think she is to encourage this type of offer?" Well, the fact is that the market has not slowed down in 2017 and prices thus far have surpassed what folks paid in 2016. Essentially, if you bought last year, you are ahead of the game.

But let's be honest: The market can soften and values can decline. This is real estate, a commodity that fluctuates just like other investments. If you are buying in this market and are only considering certain areas, you will likely need to pay a premium, but the key is to do so wisely. Purchase a property that will fit your needs for the next 7 to 10 years or more. That way, you won't have to worry about the market going up or down because you won't be selling. Furthermore, the market may soften, but interest rates will likely go up.

This morning I was talking with Vanessa Bergmark, the owner of Red Oak, about our market's similarities with the stock market. Let's say you invest in a retirement account with a goal of retiring in 2030. You may work with an advisor or select mutual funds based upon moderate growth. You may see retirement rise and fall, but you do not panic because you're not retiring anytime soon. You would not do a panic sale at the threat of further decline; you would wait it out. You should have the same outlook when buying a home: Buy a place you can afford that fits your needs and is in a neighborhood that works for you. Enjoy life and hold on to your property.

I have heard many buyers say they would never pay that much for that house and, just like that, values increase even more. Earlier this year, I had clients who were trying to buy a home in South Berkeley but did not want to spend more than $950,000. They wrote a $950k offer and were verbally countered to $990,000. They decided to liquidate some assets and stretch to the $990,000 price in order to buy the home. Fast forward 6 weeks later, a home within 1 block closed escrow at $1,200,000. By stretching in that moment, those buyers scored a home that they love and have stopped chasing the market. If you're currently looking to buy and are not offering enough money, you are chasing the market with your next offer.

Five years ago, I helped someone buy a fixer in the Rose Garden area of Oakland. At the time, I worried that they overpaid. (Yes, I worry all of the time for my clients!) For that year, they paid top dollar for a home in that condition, yet one year later a home half the size on the same block sold for $100,000 more than what they paid. Fast forward, 3 more years and they are ahead by $250,000.

This is not to say that you should buy a lemon or buy beyond your means; rather, focus on what you can afford. Buy smart and for the long haul.

Home Buyer Q & A

Q: What are some common costs home buyers overlook when purchasing a house?

A: One of the first things I talk to clients about is expectations. Often buyers look at homes that are freshly painted and appear updated and the assumption is that everything is done or is turn-key. In our marketplace I tell clients to expect about $30,000 in repair recommendations. It could be a sewer line that needs to be replaced, an old roof, a bad electrical panel or foundation work. A huge portion of my clients last year needed to replace Federal Pacific electrical panels; a very common panel in homes built in the mid-century. Often electrical work is a recommended “do now” repair. Another common misconception is that a buyer will pay property taxes based upon the current owners tax basis. Yes, as part of the buyer’s closing costs, they will be billed at the current owner’s property tax, however within 6-10 months buyers will receive a supplemental tax bill that is a retroactive bill from the date of closing, which is the difference between the previous owner’s tax bill and the current tax bill. Therefore if the seller paid $5,000 per year in property taxes and the current tax bill is $10,000 a buyer will owe the difference. Property taxes are based upon your purchase price; 1% of the purchase price, plus another fraction of a percentage (that varies city to city), which is derived from bonds and assessments.

Another surprise to some buyers is that seismic retrofitting is currently considered an upgrade. The bolting, shear wall support and bracing to help protect a home in an earthquake is an upgrade, meaning a buyer will likely want to budget for this work and not expect it. Let's say a home is built in the 1940s and there are bolts in place, those bolts are very likely not up to today's standards and are considered undersized. Year by year we know much more about earthquake safety, as well as more about where fault lines are.

Q: Are any costs associated with buying a house negotiable? How can you go about negotiating those or secure lower costs?

A: Everything in a real estate transaction is negotiable, however, in the robust Oakland-Berkeley marketplace, the vast majority of closing cost fees are customary "pre-assigned". I have seen heavy cash down or all cash buyers pay seller closing costs in an effort to reduce the purchase price. By doing this they hope to have a slightly lower property tax basis. The one thing that should be known is the city may call and ask questions about the transaction and I have heard that there is no guarantee that the city may not adjust the value up.

Q: What are some more common costs associated with owning a home that you wouldn't experience through renting?

A: You will need to fix all repairs, there is no landlord to call when the hot water heater breaks or the roof leaks.

Q: What are some of the best ways to financially prepare for buying a house?

A: Do not spend all of your liquid assets getting into a home nor use them as your down payment. Make sure you work with a mortgage lender who provides spreadsheets of all of the out-of-pocket expenses, monthly payments, property taxes, etc. Plug those numbers into your budget. See if you have money to eat a meal out, fix an unexpected repair or make the improvements that you desire. The best strategy would be to have a house savings fund for future repairs and maintenance, almost like an HOA reserve fund. I have done a home improvement project almost every year that I have owned my house.

Brokers Tour Very Special Find of the Day

Listed by Martha Hill of Pacific Union International

First time on the market in 55 years. 25 Lexford Place in Oakland is a very special home.

Brokers Tour Find of the Day

Listed by Sexton Group, Ernie Sexton

1 Ronada Ave., Oakland

Favorite Things: No.1

I threw together a list of some of my favorite things for fun. Some are free, some are luxe, I thought I would share a piece of me. Drop me a line and let me know your favorite things!

Answering buyer questions regarding mortgage financing

A first-time buyer reached out to me with some great questions. They are looking to buy a house in Berkeley or Oakland within the next year and had already pursued mortgage financing with a “big bank” as well as a local mortgage lender for a loan pre-approval. With their price point being $700k-$800k and a 20% down payment, they received rates for a 30-year fixed loan that varied from 3.875% from a “big bank” to 4.7% from a local lender. They also had an option utilizing cash through a source that would take some time to acquire.

They wanted to know my thoughts on, 1) buying a loan vs. buying cash, and 2) working with a local lender versus a “big bank.” My response to them was:

One of the drivers of our market in the last 4 years has been low inventory, which has created multiple offers. I track approximately 200+ transactions in the Oakland and Berkeley area annually and, what is important to note, approximately 80% of winning offers are written with the buyers waiving all of their contingencies (online tools do not reveal type of financing or terms of the winning offers). If the property is popular, it can be a battleground situation. One of the implications to this type of offer is that your initial down payment (typically 3% of the offer price) is at risk if you do not close escrow for any reason.

As far as big bank versus local lender, in the 12 years of selling hundreds of homes the majority of my transactions are with local mortgage brokers doing the financing (with a handful of exceptions), but never with the big bank financial institution that this particular buyer solicited. Typically in this multiple offer market, a seller will go with the known quantity, meaning the local Realtor and local mortgage lender whose reputations for closing deals precede them.

An example being, this year my client purchased a 2 bedroom, 2 bathroom penthouse in the Adams Point neighborhood of Oakland. On this property there were 12 offers received and there was a full day of negotiating. There were 4 offers that received a multiple counter offer from the seller. In the end my client had to increase her price to win the deal, but I found out afterwards that there was another offer identical to ours. The listing agent mentioned to me that the sellers picked my client’s offer because she conveyed to her seller that I was a local agent with a vast amount of experience in our market and the lender was a local Oakland mortgage provider. The terms and price were the same. In no way do I want my clients paying a higher interest rate by selecting a local lender over a big financial institution but we are in a market that is currently beyond competitive.

In regards to cash versus loan, cash can beat out other offers as long as it is about the same offer price as the loan offers. Meaning if there is a choice of a strong offer with a loan that is more money than a cash offer, I have seen sellers take the loan offer to yield more money. Cash is king only to a certain point. I see cash deals about 25% of the time; however, what is even more important is the reputation of your agent and lender.

I hope this potential buyer Q&A helps you as you decide your mortgage financing.

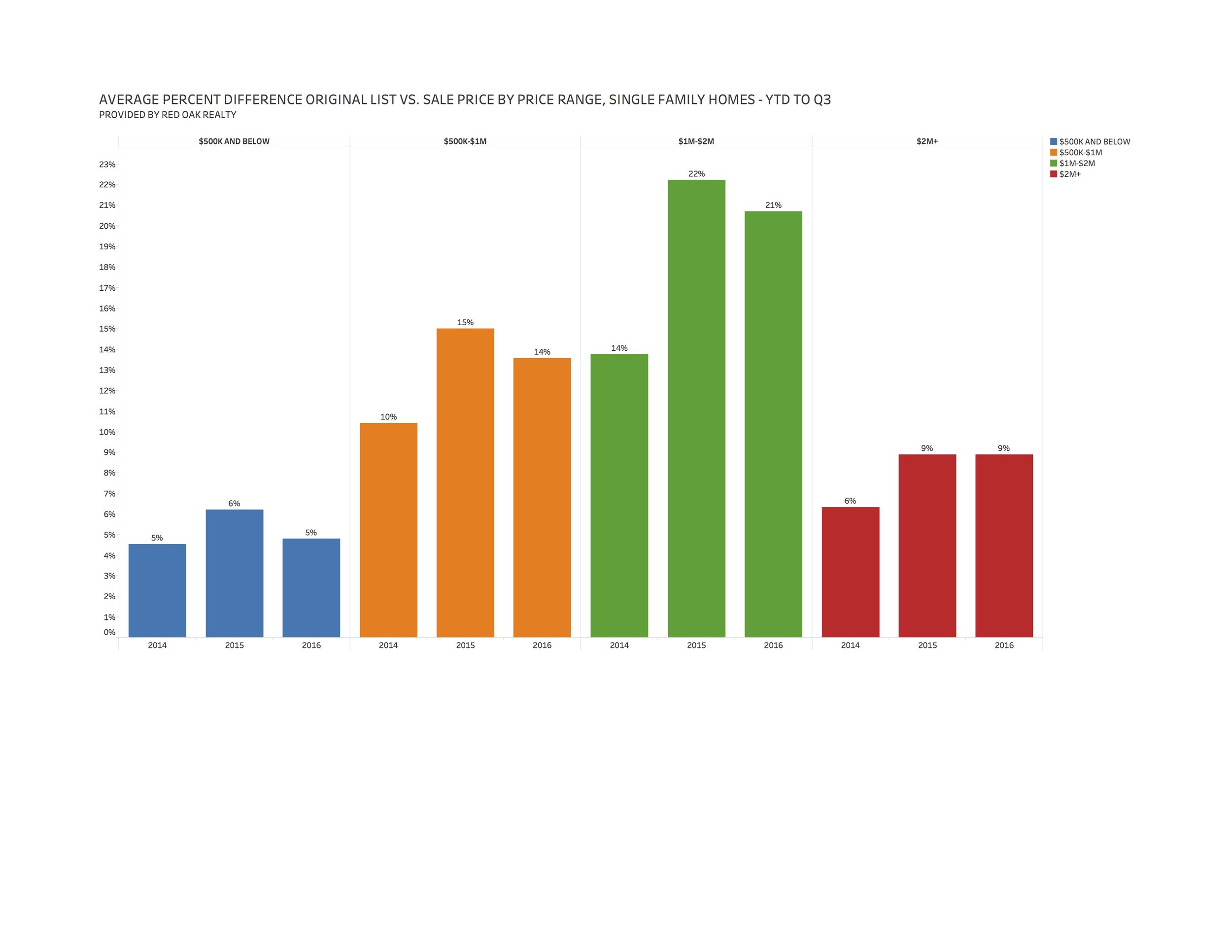

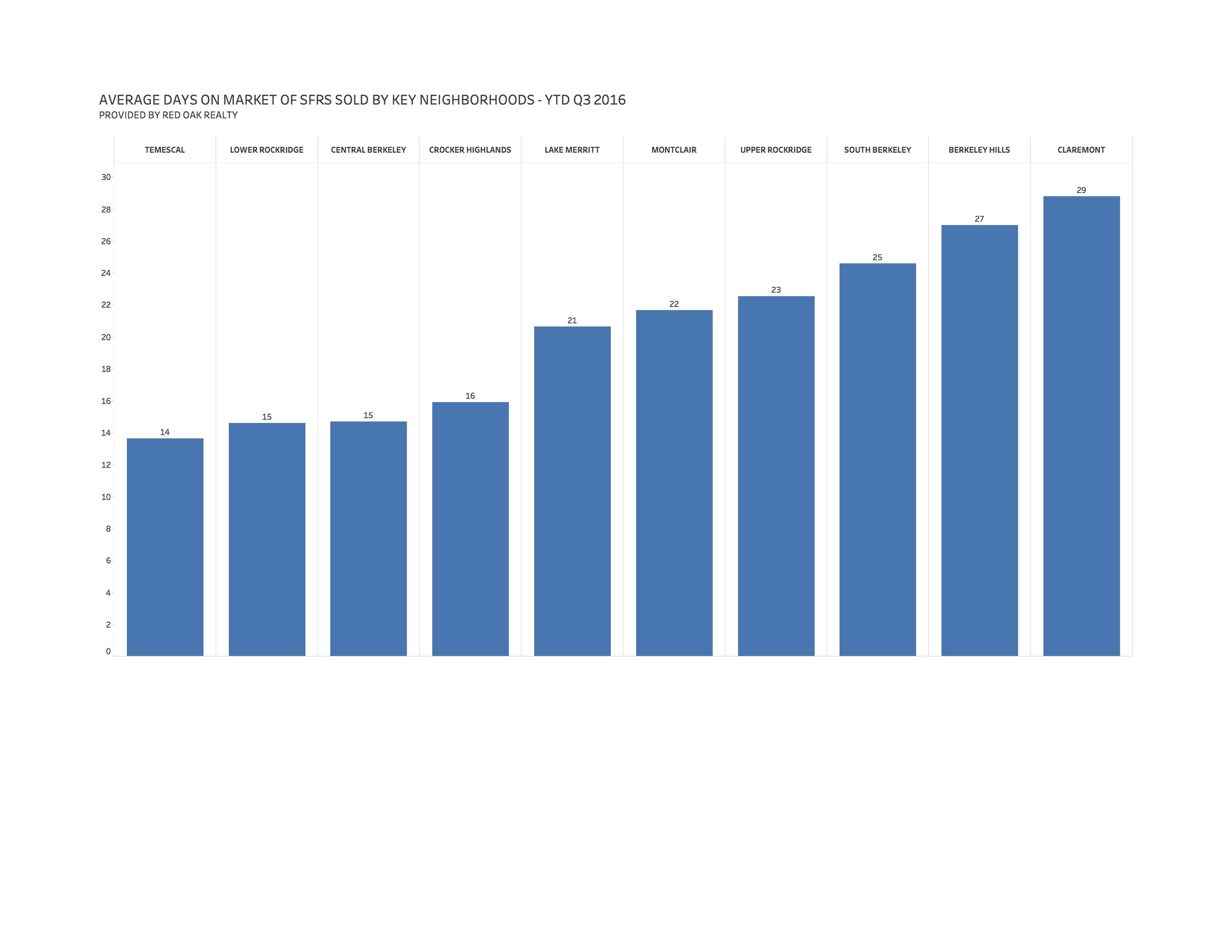

3rd Quarter Stats

Here is 2016's 3rd quarter analysis. This data is great, and is one of many tools that I use to help clients navigate our real estate market.

To Buy or Not to Buy

Yesterday I received an email from a buyer who expressed that they were discouraged by the market and were considering taking a year-long break from the house hunt. They thought the time off would be good to reassess things and watch what happens in the next year with the housing market. I completely understand their feelings. In my experience, one of the biggest causes of frustration for buyers is the list price to sold price ratios. When you see that a home sold for 30% to 40% over the asking price it is sure to be a huge wet blanket. Often times in those vast scenarios, the house was dreadfully underpriced. It would be less discouraging if you saw something priced at $1.250 million and then see it close at $1.4 million as opposed to (this real life example of a recent sale in Montclair) a list price of $928K and selling over $1.4 million.

In regards to my buyer taking a break for a year, I support whatever decision is best for my clients. I am a big believer in buying smart and only when a house really fits your needs. My best advice would be to line up your financing and be open to what the market may bring, but not feel pressed to buy for the sake of buying. Next year may bring us a different market and we will not know until we are actively in it. Perhaps set a pause button but stay open to the possibilities that may come.

Favorite Find on Brokers Tour - Church Re-Do

Source: The Home Co. Realtors

751 47th St, Oakland

3,845 sq ft | List Price $899,000

Waiving an Appraisal Contingency

If you are active in the Oakland, Berkeley real estate market then you are aware we are in a seller's market and you have likely heard about all of the non-contingent offers. In a seller’s market there are typically multiple bids on a property. When a buyer writes a competitive offer in an attempt to win the bidding war there are three main contingencies to consider; the inspection contingency, loan contingency, and appraisal contingency. These contingencies are in place to protect the buyer, however, a buyer can choose to waive any or all in an effort to strengthen their offer and make it more appealing to the seller. I write many non-contingent offers for clients but I only do this when my clients have a thorough understanding of the risks and implications involved with writing and submitting a non-contingent offer.

When writing an offer with no contingencies, you are telling the seller that should you cancel, for any reason, you are aware that you are at risk of losing your earnest/initial deposit money.

Because the appraisal is an aspect of the escrow that is determined by a third party, I'd like to further address the appraisal contingency in more detail. Every house purchased with a loan has an appraisal performed. The hope is that the property appraises at the offer price. Sometimes, in a seller’s market, bidding wars can cause appraisals to come in lower than the purchase price. When an appraisal contingency is in place, an appraisal that comes in lower than the contracted purchase price allows the buyer the opportunity to potentially renegotiate the offer price with the seller. In contrast, if a buyer decides to waive the appraisal contingency, they have to be prepared to increase their down payment to cover the difference in the appraised value and their offer price.

Real World Example:

You are offering $900,000 on a home and it is your goal to buy a home with a 20% down-payment ($180,000 cash/$720,000 loan).

The appraiser comes out and appraises the home at $880,000. You have waived your appraisal contingency, so you will need to have funds to cover the 20% down-payment, of the appraisal price ($176,000) plus an additional $20,000. See below:

$176,000 adjusted down-payment based upon 20% of the appraisal value +

$20,000 additional down-payment +

$704,000 adjusted loan amount = $900,000

Why do the numbers change? A 20% down-payment loan program is based upon the appraised value, not the offer price. The seller accepted your offer at $900,000 and you wrote your offer saying you would pay $900,000, even if it does not appraise at this price.

What is at stake if you take a risk and do not have the funds to cover the difference? Your earnest money, also known as a good faith deposit. Typically, in our niche market, buyers are placing 3% of their offer price in a neutral escrow account. This money is held there until the escrow officer has mutual instructions from both the buyer's agent and seller's agent. This 3% is applied to the buyer's down-payment, unless the buyer breaches their contract. "Breach" means backing out for a reason outside of your contingencies or reasons not permissible per the contract. So, if you write an offer with no contingencies, which many buyers are now doing, and you back out because an appraiser values your potential future home for less than you offer, this is considered a breach of contract.

I hope this explanation helps you better understand the risks and implications of offers written without contingencies - specifically, an appraisal contingency.

Welcoming the Fall Season with Gratitude

After a busy first half of the year, August greeted me with a slightly more relaxed schedule, which was a blessing because I am gearing up for what I think will be a robust September. Currently I have several buyers looking for homes and several homes getting prepped to hit the market. As I review my business it feels good because it is balanced; there are qualified buyers in search of their next abode and lovely homes getting the final touches to impress their next stewards. When I reflect on my book of business it is so much more than closed deals, it is about the people. Every transaction has a personal story, a life change, a new adventure, and a new beginning. I am so grateful that you share a piece of your life with me!

Last night I was invited over to my clients Lindsay, Kelly and Collins’s home for wine and cheese. It has been less than two months since they closed escrow and they have already put their mark on their new space. One of my recommended arborists came and sculpted the trees that were long overdue for pruning, the wood paneled walls (not the good kind) were removed and replaced with crisp Dove White paint, the light fixtures that were replaced with Rejuvenation lighting (I am able to pass along my trade discount for my clients!), the living room furniture was ordered and delivered, a once-dated fireplace was updated with a wall of white brick, the older Formica and wood bar was transformed with crisp subway tiles installed in a herringbone design, and the bar sink was capped with Carrera marble! After a tour of their home I was handed a chilled glass of rosé and a cheese platter was served. It was so nice to relax and learn more about my clients. After what felt like a brief visit, but was actually 4 hours, I drove home and was filled with gratitude to have people come into my life and stay.

Why do I share my personal tidbits with you? Because you share your hopes, dreams and fears with me. This fall season’s big news is my beloved assistant Kelly is getting married! I am very excited for her as she marries the love of her life. My youngest, my son Miles, just started his senior year of high school. He is a team captain on his football team so on game days I will be screaming for the Saint Mary's Panthers!

My son is #17 Photo credit: James Jackson

This month marks my 12th year in business and I want to thank you, my husband, daughter, son, Kelly and the entire Red Oak staff for the ride!

Happy fall season!

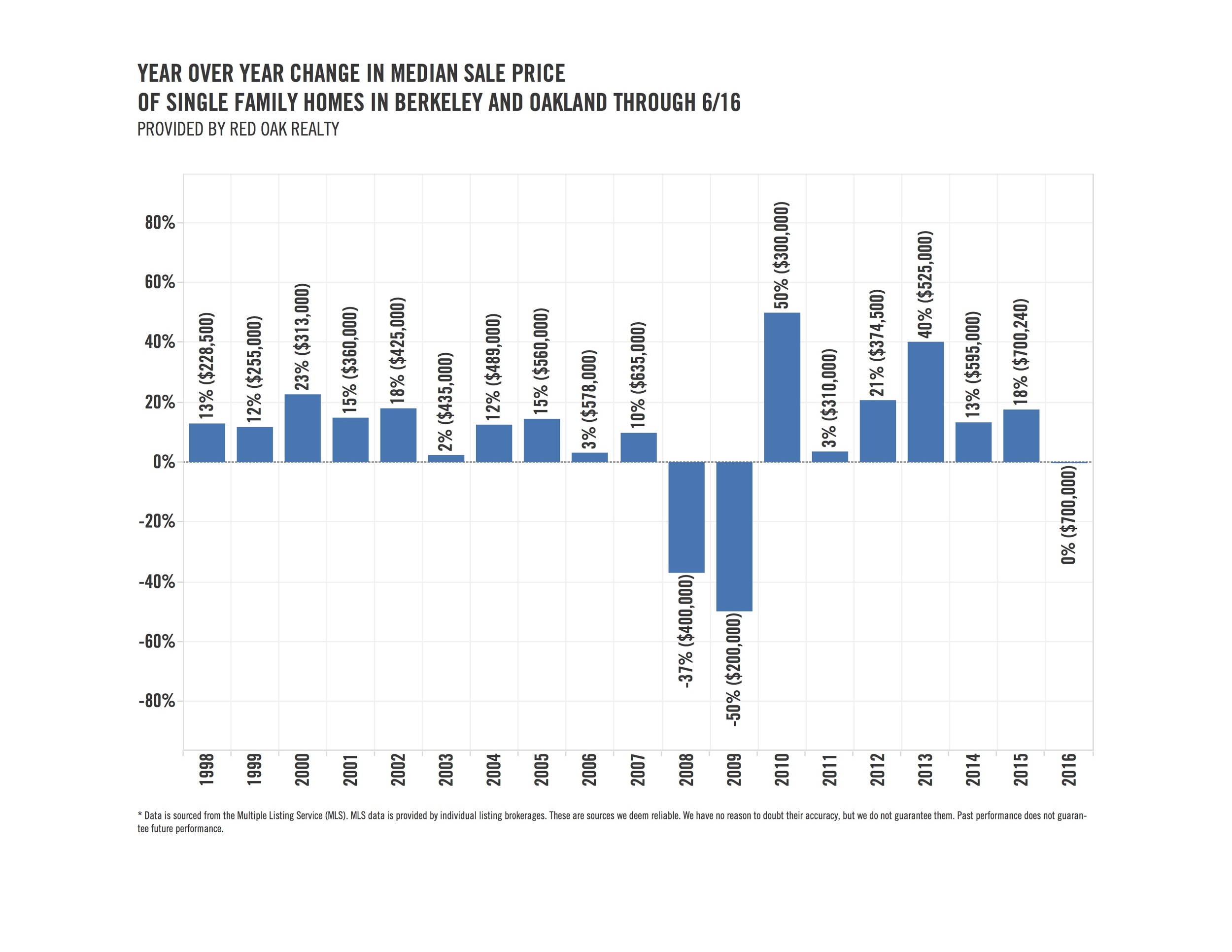

Will My Home Appreciate?

Many people ask me, "Is this a bubble...when will it burst?" So I thought, let's track appreciation versus depreciation in the Oakland and Berkeley real estate market. I tracked sales posted on the local multiple listing service (MLS) back to 1998 and it turns out that we only had 2 years of depreciation, 2008 and 2009. Funny, I remember that the Federal government gave an $8,000 first-time-buyer tax incentive in 2009/2010 that really boosted sales; and we have not looked back.

We cannot predict how future markets will pan out appreciation-wise, but it is good to know that going back 18 years there has been only 2 years of depreciation. This is good data to use in your decision on if or when you should buy.

Broker Tour Find of the Day

Source: Pacific Union, Jackie Care, Listing Agent

A True Artist's Home - lluminating with style

2974 Burdeck Drive